단순선형 회귀 Simple Linear Regression

: ols()

: 독립변수 - 연속형, 종속변수 - 연속형.

: 독립변수 1개

* linear_reg4.py

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

plt.rc('font', family='malgun gothic')

df = pd.read_csv('../testdata/drinking_water.csv')

print(df.head(3), '\n', df.describe())

'''

친밀도 적절성 만족도

0 3 4 3

1 3 3 2

2 4 4 4

'''

print(df.corr()) # 적절성/만족도 상관계수 : 0.766853

print('----------------------------------------------------------------------')

import statsmodels.formula.api as smf

model = smf.ols(formula='만족도 ~ 적절성', data=df).fit()

print(model.summary()) OLS Regression Results

==============================================================================

Dep. Variable: 만족도 R-squared: 0.588

Model: OLS Adj. R-squared: 0.586

Method: Least Squares F-statistic: 374.0

Date: Thu, 11 Mar 2021 Prob (F-statistic): 2.24e-52

Time: 10:07:49 Log-Likelihood: -207.44

No. Observations: 264 AIC: 418.9

Df Residuals: 262 BIC: 426.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.7789 0.124 6.273 0.000 0.534 1.023

적절성 0.7393 0.038 19.340 0.000 0.664 0.815

==============================================================================

Omnibus: 11.674 Durbin-Watson: 2.185

Prob(Omnibus): 0.003 Jarque-Bera (JB): 16.003

Skew: -0.328 Prob(JB): 0.000335

Kurtosis: 4.012 Cond. No. 13.4

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.[해석]

상관계수 ** 2 = 결정계수

print(0.766853 ** 2) # 0.588063523609

R-squared : 결정계수(설명력), 상관계수 R의 제곱 : 0.588

: 1 - (SSE(explain sum of square-추세선과 데이터간 y값) / SST(total sum of square - 평균과 추세선간 y값

차이) )

: 1 - (SSE / SST)

=> over fitting : R2가 1에 아주 가까우면(기존 데이터와 추사) 새로운 데이터에 대해 설명력이 좋지않다.

적절성의 p-value : 0.000 < 0.05 => 모델은 유효하다.

std err(표준 오차) : 0.038

Intercept(y절편) : 0.7789

coef(기울기) : 0.7393

t = 기울기/ 표준오차 : 19.340

print(0.7393 / 0.038) # 19.455263157894738

F-statistic = t**2 : 374.0

print(19.340 ** 2) # 374.0356

독립변수가 많을 경우 R-squared과 Adj. R-squared의 차이가 클 경우 독립변수 이상치를 확인해야한다.

Kurtosis : 4.012 => 3보다 클경우 평균에 데이터가 몰려있다.

print(model.params) # y절편과 기울기 산출

# Intercept 0.778858

#적절성 0.739276

print(model.rsquared) # 0.5880630629464404

print()

print(model.pvalues)

'''

Intercept 1.454388e-09

적절성 2.235345e-52

'''

#print(model.predict()) # 예측값

print(df.만족도[0],' ', model.predict()[0]) # 3 3.7359630488589186

# 새로운 값 예측

print(df.적절성[:5])

'''

3 3.7359630488589186

0 4

1 3

2 4

3 2

4 2

'''

print(df.만족도[:5])

'''

0 3

1 2

2 4

3 2

4 2

'''

print(model.predict()[:5]) # [3.73596305 2.99668687 3.73596305 2.25741069 2.25741069]

print()

new_df = pd.DataFrame({'적절성':[6,5,4,3,22]})

new_pred = model.predict(new_df)

print('new_pred :\n', new_pred)

'''

0 5.214515

1 4.475239

2 3.735963

3 2.996687

4 17.042934

'''

plt.scatter(df.적절성, df.만족도)

slope, intercept = np.polyfit(df.적절성, df.만족도, 1) # R의 abline 기능

plt.plot(df.적절성, df.적절성 * slope + intercept, 'b') # 추세선

plt.show()

다중 선형회귀 Multiple Linear Regression

: 독립변수가 복수

model2 = smf.ols(formula='만족도 ~ 적절성 + 친밀도', data=df).fit()

print(model2.summary()) OLS Regression Results

==============================================================================

Dep. Variable: 만족도 R-squared: 0.598

Model: OLS Adj. R-squared: 0.594

Method: Least Squares F-statistic: 193.8

Date: Thu, 11 Mar 2021 Prob (F-statistic): 2.61e-52

Time: 11:19:33 Log-Likelihood: -204.37

No. Observations: 264 AIC: 414.7

Df Residuals: 261 BIC: 425.5

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.6673 0.131 5.096 0.000 0.409 0.925

적절성 0.6852 0.044 15.684 0.000 0.599 0.771

친밀도 0.0959 0.039 2.478 0.014 0.020 0.172

==============================================================================

Omnibus: 13.103 Durbin-Watson: 2.174

Prob(Omnibus): 0.001 Jarque-Bera (JB): 17.256

Skew: -0.382 Prob(JB): 0.000179

Kurtosis: 3.992 Cond. No. 18.8

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.단순 선형 회귀

: iris dataset, ols() 사용. 상관관계가 약한/강한 변수로 모델 작성.

* linear_reg5.py

import pandas as pd

import statsmodels.formula.api as smf

import seaborn as sns

iris = sns.load_dataset('iris')

print(iris.head(3))

'''

sepal_length sepal_width petal_length petal_width species

0 5.1 3.5 1.4 0.2 setosa

1 4.9 3.0 1.4 0.2 setosa

2 4.7 3.2 1.3 0.2 setosa

'''

print(iris.corr())

'''

sepal_length sepal_width petal_length petal_width

sepal_length 1.000000 -0.117570 0.871754 0.817941

sepal_width -0.117570 1.000000 -0.428440 -0.366126

petal_length 0.871754 -0.428440 1.000000 0.962865

petal_width 0.817941 -0.366126 0.962865 1.000000

'''# 단순 선형회귀 모델 : 상관관계 r = -0.117570(sepal_length/sepal_width)

result = smf.ols(formula = 'sepal_length ~ sepal_width', data=iris).fit()

#print(result.summary()) # R2 : 0.014

print(result.rsquared)# 0.01382 < 0.05 => 의미없는 모델

print(result.pvalues) # 1.518983e-01 > 0.05result2 = smf.ols(formula = 'sepal_length ~ petal_length', data=iris).fit()

print(result2.summary()) # R2 : 0.760 => 설명력

print(result2.rsquared)# 0.7599 > 0.05 => 의미있는 모델

print(result2.pvalues) # 1.038667e-47 < 0.05

print()

pred = result2.predict()

print('실제값 :', iris.sepal_length[0]) # 실제값 : 5.1

print('예측값 :', pred[0]) # 예측값 : 4.879094603339241

# 새로운 데이터로 예측

print(iris.petal_length[1:5])

new_data = pd.DataFrame({'petal_length':[1.4, 0.5, 8.5, 12.123]})

print(new_data)

'''

petal_length

0 1.400

1 0.500

2 8.500

3 12.123

'''

y_pred_new = result2.predict(new_data)

print('새로운 데이터로 sepal_length예측 :\n', y_pred_new)

'''

0 4.879095

1 4.511065

2 7.782443

3 9.263968

'''

다중 선형 회귀

result3 = smf.ols(formula = 'sepal_length ~ petal_length + petal_width', data=iris).fit()

print(result3.summary()) # R2 : 0.760 => 설명력 OLS Regression Results

==============================================================================

Dep. Variable: sepal_length R-squared: 0.766

Model: OLS Adj. R-squared: 0.763

Method: Least Squares F-statistic: 241.0

Date: Thu, 11 Mar 2021 Prob (F-statistic): 4.00e-47

Time: 12:09:43 Log-Likelihood: -75.023

No. Observations: 150 AIC: 156.0

Df Residuals: 147 BIC: 165.1

Df Model: 2

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

Intercept 4.1906 0.097 43.181 0.000 3.999 4.382

petal_length 0.5418 0.069 7.820 0.000 0.405 0.679

petal_width -0.3196 0.160 -1.992 0.048 -0.637 -0.002

==============================================================================

Omnibus: 0.383 Durbin-Watson: 1.826

Prob(Omnibus): 0.826 Jarque-Bera (JB): 0.540

Skew: 0.060 Prob(JB): 0.763

Kurtosis: 2.732 Cond. No. 25.3

==============================================================================print('R-squared :', result3.rsquared)# 0.7662 > 0.05 => 의미있는 모델

print('p-value', result3.pvalues)

# petal_length 9.414477e-13

# petal_width 4.827246e-02

# y = 0.5418 * x1 -0.3196 * x2 + 4.1906# 새로운 데이터로 예측

new_data2 = pd.DataFrame({'petal_length':[8.5, 12.12], 'petal_width':[8.5, 12.5]})

y_pred_new2 = result3.predict(new_data2)

print('새로운 데이터로 sepal_length예측 :\n', y_pred_new2)

'''

0 6.079508

1 6.762540

'''

선형 회귀 분석

: mtcars dataset, ols() 사용. 모델작성 후 추정치 얻기

* linear_reg6.py

import statsmodels.api

import statsmodels.formula.api as smf

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

plt.rc('font', family='malgun gothic')

mtcars = statsmodels.api.datasets.get_rdataset('mtcars').data

print(mtcars)

'''

mpg cyl disp hp drat ... qsec vs am gear carb

Mazda RX4 21.0 6 160.0 110 3.90 ... 16.46 0 1 4 4

Mazda RX4 Wag 21.0 6 160.0 110 3.90 ... 17.02 0 1 4 4

'''

print(mtcars.columns) # Index(['mpg', 'cyl', 'disp', 'hp', 'drat', 'wt', 'qsec', 'vs', 'am', 'gear', 'carb'], dtype='object')

print(mtcars.describe())

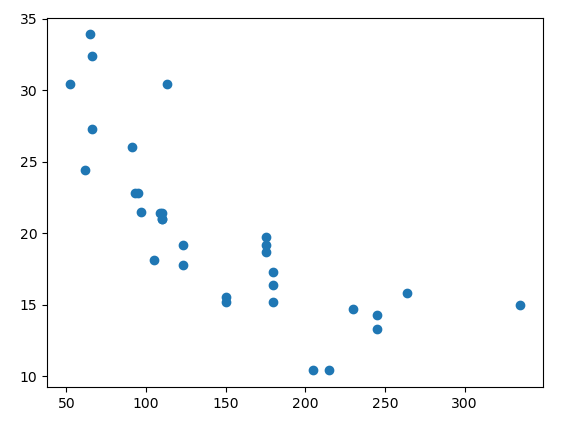

print(np.corrcoef(mtcars.hp, mtcars.mpg)) # 상관계수 : -0.77616837

print(np.corrcoef(mtcars.wt, mtcars.mpg)) # 상관계수 : -0.86765938

print(mtcars.corr())# 시각화

plt.scatter(mtcars.hp, mtcars.mpg)

plt.xlabel('마력 수')

plt.ylabel('연비')

slope, intercept = np.polyfit(mtcars.hp, mtcars.mpg, 1) # 1차원

plt.plot(mtcars.hp, mtcars.hp * slope + intercept, 'r')

plt.show()

# 단순선형 회귀

result = smf.ols('mpg ~ hp', data=mtcars).fit()

print(result.summary())

print(result.conf_int(alpha=0.05)) # 33.435772

print(result.summary().tables[0]) # coef * x + Intercept

print('마력수 110에 대한 연비 예측 :', -0.0682 * 110 + 30.0989) # 22.5969

print('마력수 50에 대한 연비 예측 :', -0.0682 * 50 + 30.0989) # 26.6889

# 마력이 증가하면 연비는 줄어든다. 음의 상관관계이므로 결과는 반비례한다. 참고 자료로만 활용해야한다.# 다중선형 회귀

result2 = smf.ols('mpg ~ hp + wt', data=mtcars).fit()

print(result2.summary())

print(result2.conf_int(alpha=0.05))

print(result2.summary().tables[0])

print('마력수 110 + 무게 5에 대한 연비 예측 :', ((-0.0318 * 110) +(-3.8778 * 5) + 37.2273)) # 14.3403print('추정치 구하기 차체 무게를 입력해 연비를 추정')

result3 = smf.ols('mpg ~ wt', data=mtcars).fit()

print(result3.summary())

print('결정계수 :', result3.rsquared) # 0.7528327936582646 > 0.05 설명력이 우수한 모델

pred = result3.predict()# 1개의 자료로 실제값과 예측값(추정값) 저장 후 비교

print(mtcars.mpg[0])

print(pred[0]) # 모든 자동차 차체 무게에 대한 연비 추정치 출력

data = {

'mpg':mtcars.mpg,

'mpg_pred':pred

}

df = pd.DataFrame(data)

print(df)

'''

mpg mpg_pred

Mazda RX4 21.0 23.282611

Mazda RX4 Wag 21.0 21.919770

Datsun 710 22.8 24.885952

'''# 새로운 차체 무게로 연비 추정하기

mtcars.wt = float(input('차체 무게 입력:'))

new_pred = result3.predict(pd.DataFrame(mtcars.wt))

print('차체 무게 {}일때 예상연비{}이다'.format(mtcars.wt[0], new_pred[0]))

# 차체 무게 1일때 예상연비31.940654594619367이다# 여러 차제 무게에 대한 연비 추정

new_wt = pd.DataFrame({'wt':[6, 3, 0.5]})

new_pred2 = result3.predict(pd.DataFrame(new_wt))

print('예상연비 : \n', np.round(new_pred2.values, 2)) # [ 5.22 21.25 34.61]선형 회귀 분석

: 여러매체의 광고비에 따른 판매량 데이터, ols() 사용. 모델작성 후 추정치 얻기

* linear_reg7

import statsmodels.api

import statsmodels.formula.api as smf

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

adf_df = pd.read_csv('../testdata/Advertising.csv', usecols=[1,2,3,4])

print(adf_df.head(3), ' ', adf_df.shape) # (200, 4)

print(adf_df.index, adf_df.columns)

print(adf_df.info())

'''

tv radio newspaper sales

0 230.1 37.8 69.2 22.1

1 44.5 39.3 45.1 10.4

2 17.2 45.9 69.3 9.3

'''

print('상관계수 r : \n', adf_df.loc[:, ['sales', 'tv']].corr())

'''

sales tv

sales 1.000000 0.782224

tv 0.782224 1.000000

'''

# r : 0.782224 > 0.05 => 강한 양의 상관관계이고, 인과관계임을 알 수 있다.

print()

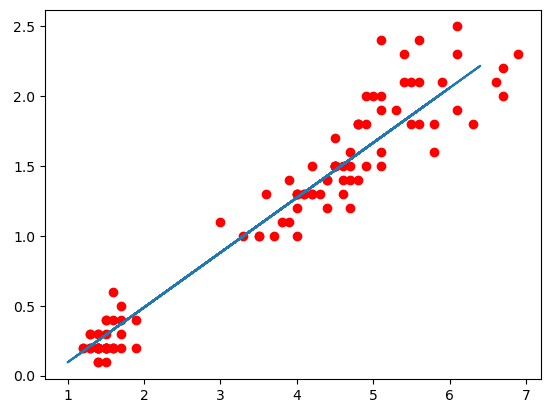

lm = smf.ols(formula='sales ~ tv', data=adf_df).fit()

print(lm.summary()) # R-squared : 0.612, p : 1.47e-42

print(lm.params)

print(lm.pvalues)

print(lm.rsquared)# 시각화

plt.scatter(adf_df.tv, adf_df.sales)

plt.xlabel('tv')

plt.ylabel('sales')

x = pd.DataFrame({'tv':[adf_df.tv.min(), adf_df.tv.max()]})

y_pred = lm.predict(x)

plt.plot(x, y_pred, c='red')

plt.title('Linear Regression')

sns.regplot(adf_df.tv, adf_df.sales, scatter_kws = {'color':'r'})

plt.xlim(-50, 350)

plt.ylim(ymin=0)

plt.show()

# 예측 : 새로운 tv값으로 sales를 추정

x_new = pd.DataFrame({'tv':[230.1, 44.5, 100]})

pred = lm.predict(x_new)

print('추정값 :\n', pred)

'''

0 17.970775

1 9.147974

2 11.786258

'''print('\n다중 선형회귀 모델 ')

lm_mul = smf.ols(formula = 'sales ~ tv + radio + newspaper', data = adf_df).fit()

# + newspaper 포함시와 미포함시의 R2값 변화가 없어 제거 필요.

print(lm_mul.summary())

print(adf_df.corr())

# 예측2 : 새로운 tv, radio값으로 sales를 추정

x_new2 = pd.DataFrame({'tv':[230.1, 44.5, 100], 'radio':[30.1, 40.1, 50.1],\

'newspaper':[10.1, 10.1, 10.1]})

pred2 = lm.predict(x_new2)

print('추정값 :\n', pred2)

'''

0 17.970775

1 9.147974

2 11.786258

'''회귀분석모형의 적절성을 위한 조건

: 아래의 조건 위배 시에는 변수 제거나 조정을 신중히 고려해야 함.

- 정규성 : 독립변수들의 잔차항이 정규분포를 따라야 한다.

- 독립성 : 독립변수들 간의 값이 서로 관련성이 없어야 한다.

- 선형성 : 독립변수의 변화에 따라 종속변수도 변화하나 일정한 패턴을 가지면 좋지 않다.

- 등분산성 : 독립변수들의 오차(잔차)의 분산은 일정해야 한다. 특정한 패턴 없이 고르게 분포되어야 한다.

- 다중공선성 : 독립변수들 간에 강한 상관관계로 인한 문제가 발생하지 않아야 한다.

# 잔차항

fitted = lm_mul.predict(adf_df) # 예측값

print(fitted)

'''

0 20.523974

1 12.337855

2 12.307671

'''

residual = adf_df['sales'] - fitted # 잔차

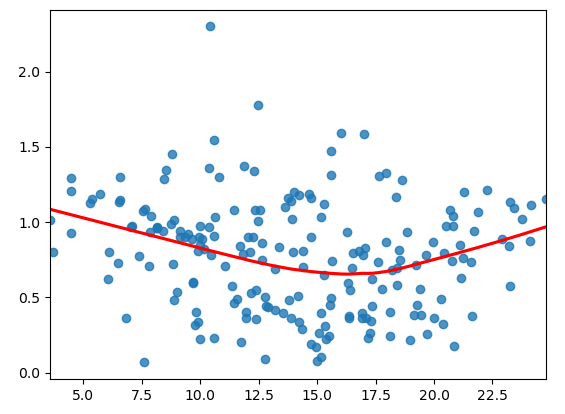

import seaborn as sns

print('선형성 - 예측값과 잔차가 비슷하게 유지')

sns.regplot(fitted, residual, lowess = True, line_kws = {'color':'red'})

plt.plot([fitted.min(), fitted.max()], [0, 0], '--', color='grey')

plt.show() # 선형성을 만족하지 못한다.

print('정규성- 잔차가 정규분포를 따르는 지 확인')

import scipy.stats as stats

sr = stats.zscore(residual)

(x, y), _ = stats.probplot(sr)

sns.scatterplot(x, y)

plt.plot([-3, 3], [-3, 3], '--', color="grey")

plt.show() # 선형성을 만족하지 못한다.

print('residual test :', stats.shapiro(residual))

# residual test : ShapiroResult(statistic=0.9176644086837769, pvalue=3.938041004403203e-09)

# pvalue=3.938041004403203e-09 < 0.05 => 정규성을 만족하지못함.

print('독립성 - 잔차가 자기상관(인접 관측치의 오차가 상관되어 있음)이 있는지 확인')

# 모델.summary() Durbin-Watson:2.084 => 잔차항이 독립성을 만족하는 지 확인. 2에 가까우면 자기상관이 없다.(서로 독립- 잔차끼리 상관관계가 없다)

# 0에 가까우면 양의 상관, 4에 가까우면 음의 상관.print('등분산성 - 잔차의 분산이 일정한지 확인')

sns.regplot(fitted, np.sqrt(np.abs(sr)), lowess = True, line_kws = {'color':'red'})

plt.show()

# 추세선이 수평선을 그리지않으므로 등분산성을 만족하지 못한다.

print('다중공선성 - 독립변수들 간에 강한 상관관계 확인')

# VIF(Variance Inflation Factors - 분산 팽창 요인) 값이 10을 넘으면 다중공선성이 발생하는 변수라고 할 수 있다.

from statsmodels.stats.outliers_influence import variance_inflation_factor

print(variance_inflation_factor(adf_df.values, 0)) # 23.198876299003153

print(variance_inflation_factor(adf_df.values, 1)) # 12.570312383503682

print(variance_inflation_factor(adf_df.values, 2)) # 3.1534983754953845

print(variance_inflation_factor(adf_df.values, 3)) # 55.3039198336228

# DataFrame으로 보기

vif_df = pd.DataFrame()

vif_df['vid_value'] = [variance_inflation_factor(adf_df.values, i) for i in range(adf_df.shape[1])]

print(vif_df)

'''

vid_value

0 23.198876

1 12.570312

2 3.153498

3 55.303920

'''print('참고 : cooks distance - 극단값을 나타내는 지료 확인')

from statsmodels.stats.outliers_influence import OLSInfluence

cd, _ = OLSInfluence(lm_mul).cooks_distance

print(cd.sort_values(ascending=False).head())

'''

130 0.272956

5 0.128306

75 0.056313

35 0.051275

178 0.045921

'''

import statsmodels.api as sm

sm.graphics.influence_plot(lm_mul, criterion='cooks')

plt.show()

print(adf_df.iloc[[130, 5, 75, 35, 178]]) # 극단 값으로 작업에서 제외 권장.

'''

tv radio newspaper sales

130 0.7 39.6 8.7 1.6

5 8.7 48.9 75.0 7.2

75 16.9 43.7 89.4 8.7

35 290.7 4.1 8.5 12.8

178 276.7 2.3 23.7 11.8

'''

* linear_reg8.py

from sklearn.linear_model import LinearRegression

import statsmodels.api

mtcars = statsmodels.api.datasets.get_rdataset('mtcars').data

print(mtcars[:3])

'''

mpg cyl disp hp drat wt qsec vs am gear carb

Mazda RX4 21.0 6 160.0 110 3.90 2.620 16.46 0 1 4 4

Mazda RX4 Wag 21.0 6 160.0 110 3.90 2.875 17.02 0 1 4 4

Datsun 710 22.8 4 108.0 93 3.85 2.320 18.61 1 1 4 1

'''

# hp(마력수)가 mpg(연비)에 영향을 미치지는 지, 인과관계가 있다면 연비에 미치는 영향값(추정치, 예측치)을 예측 (정량적 분석)

x = mtcars[['hp']].values

y = mtcars[['mpg']].values

print(x[:3])

'''

[[110]

[110]

[ 93]]

'''

print(y[:3])

'''

[[21. ]

[21. ]

[22.8]]

'''

import matplotlib.pyplot as plt

plt.scatter(x, y) # 산포도 출력

plt.show()

fit_model = LinearRegression().fit(x, y) # 모델 생성

print('slope :', fit_model.coef_[0]) # 기울기 : [-0.06822828]

print('intercept :', fit_model.intercept_) # y절편 : [30.09886054]

# newY = fit_model.coef_[0] * newX + fit_model.intercept_

pred = fit_model.predict(x)

print(pred[:3])

print('예측값 :', pred[:3].flatten()) # 예측값 : [22.59374995 22.59374995 23.75363068]

print('실제값 :', y[:3].flatten()) # 실제값 : [21. 21. 22.8]

print()

# 모델 성능 파악 시 R2 또는 RMSE

from sklearn.metrics import mean_squared_error

import numpy as np

lin_mse = mean_squared_error(y, pred) # 평균 제곱 오차

lin_rmse = np.sqrt(lin_mse) # 루트

print("평균 제곱 오차 : ", lin_mse) # 평균 제곱 오차 : 13.989822298268805

print("평균 제곱근 편차(RMSE) : ", lin_rmse) # 평균 제곱근 편차(RMSE) : 3.7402970868994894

print()

# 마력에 따른 연비 추정치

new_hp = [[100]]

new_pred = fit_model.predict(new_hp)

print('%s 마력인 경우 연비 추정치는 %s'%(new_hp[0][0], new_pred[0][0]))

# 100 마력인 경우 연비 추정치는 23.27603273246613선형회귀 분석 : Linear Regression

과적합 방지를 위해 Ridgo, Lasso, ElasticNet

* linear_reg9.py

import numpy as np

import pandas as pd

from sklearn.datasets import load_iris

iris = load_iris()

print(iris)

'''

[[5.1, 3.5, 1.4, 0.2],

[4.9, 3. , 1.4, 0.2],

[4.7, 3.2, 1.3, 0.2],

[4.6, 3.1, 1.5, 0.2],

[5. , 3.6, 1.4, 0.2],

[5.4, 3.9, 1.7, 0.4],

[4.6, 3.4, 1.4, 0.3],

'''

print(iris.feature_names) # ['sepal length (cm)', 'sepal width (cm)', 'petal length (cm)', 'petal width (cm)']

print(iris.target)

print(iris.target_names) # ['setosa' 'versicolor' 'virginica']

print()

iris_df = pd.DataFrame(iris.data, columns=iris.feature_names)

iris_df['target'] = iris.target

iris_df['target_names'] = iris.target_names[iris.target]

print(iris_df.head(3), ' ', iris_df.shape) # (150, 6)

'''

sepal length (cm) sepal width (cm) ... target target_names

0 5.1 3.5 ... 0 setosa

1 4.9 3.0 ... 0 setosa

2 4.7 3.2 ... 0 setosa

'''

# train / test 분리 : 과적합 방지 방법 중 1

from sklearn.model_selection import train_test_split

train_set, test_set = train_test_split(iris_df, test_size = 0.3) # data를 train 0.7, test 0.3 배율로 나눔

print(train_set.head(2), ' ', train_set.shape) # (105, 6)

print(test_set.head(2), ' ', test_set.shape) # (45, 6)# 선형회귀

# 정규화 선형회귀 방법은 선형회귀계수(weight)에 대한 제약조건을 추가함으로 해서, 모형이 과도라게 최적화(오버피팅)되는 현상을 방지할 수 있다.

from sklearn.linear_model import LinearRegression as lm

import matplotlib.pyplot as plt

print(train_set.iloc[:, [2]]) # petal.length

print(train_set.iloc[:, [3]]) # petal.width

model_ols = lm().fit(X=train_set.iloc[:, [2]], y=train_set.iloc[:, [3]])

print(model_ols.coef_[0]) # [0.41268804]

print(model_ols.intercept_) # [-0.35472987]

pred = model_ols.predict(model_ols.predict(test_set.iloc[:, [2]]))

print('ols_pred :\n', pred[:5])

'''

[[ 0.31044183]

[ 0.49464775]

[ 0.3606798 ]

[ 0.09274392]

[-0.25892194]]

'''

print('ols_real :\n', test_set.iloc[:, [3]][:5])

'''

petal width (cm)

138 1.8

143 2.3

142 1.9

79 1.0

45 0.3

'''

# 회귀분석 방법 - Ridge: alpha값을 조정(가중치 제곱합을 최소화)하여 과대/과소적합을 피한다. 다중공선성 문제 처리에 효과적.

from sklearn.linear_model import Ridge

model_ridge = Ridge(alpha=10).fit(X=train_set.iloc[:, [2]], y=train_set.iloc[:, [3]])

#점수

print(model_ridge.score(X=train_set.iloc[:, [2]], y=train_set.iloc[:, [3]])) #0.91923658601

print(model_ridge.score(X=test_set.iloc[:, [2]], y=test_set.iloc[:, [3]])) #0.935219182367

print('ridge predict : ', model_ridge.predict(test_set.iloc[:, [2]]))

plt.scatter(train_set.iloc[:, [2]], train_set.iloc[:, [3]], color='red')

plt.plot(test_set.iloc[:, [2]], model_ridge.predict(test_set.iloc[:, [2]]))

plt.show()

print('\nLasso')

# 회귀분석 방법 - Lasso: alpha값을 조정(가중치 절대값의 합을 최소화)하여 과대/과소적합을 피한다.

from sklearn.linear_model import Lasso

model_lasso = Lasso(alpha=0.1, max_iter=1000).fit(X=train_set.iloc[:, [0,1,2]], y=train_set.iloc[:, [3]])

#점수

print(model_lasso.score(X=train_set.iloc[:, [0,1,2]], y=train_set.iloc[:, [3]])) #0.921241848687

print(model_lasso.score(X=test_set.iloc[:, [0,1,2]], y=test_set.iloc[:, [3]])) #0.913186971647

print('사용한 특성수 : ', np.sum(model_lasso.coef_ != 0)) # 사용한 특성수 : 1

plt.scatter(train_set.iloc[:, [2]], train_set.iloc[:, [3]], color='red')

plt.plot(test_set.iloc[:, [2]], model_ridge.predict(test_set.iloc[:, [2]]))

plt.show()

# 회귀분석 방법 4 - Elastic Net 회귀모형 : Ridge + Lasso

# 가중치 제곱합을 최소화, 거중치 절대값의 합을 최소화, 두가지를 동시에 제약조건으로 사용

from sklearn.linear_model import ElasticNet

'BACK END > Deep Learning' 카테고리의 다른 글

| [딥러닝] 로지스틱 회귀 (0) | 2021.03.15 |

|---|---|

| [딥러닝] 다항회귀 (0) | 2021.03.12 |

| [딥러닝] 선형회귀 (0) | 2021.03.10 |

| [딥러닝] 공분산, 상관계수 (0) | 2021.03.10 |

| [딥러닝] 이항검정 (0) | 2021.03.10 |